Physical Address

5206 Hwy 5 N Suite 100, Bryant, AR, United States, Arkansas

Physical Address

5206 Hwy 5 N Suite 100, Bryant, AR, United States, Arkansas

If you are working toward the March 31 1099 e-file deadline, this is the point where small mistakes become filing problems. Many businesses think the hard part is submitting forms at the end of March. It is not. The harder part is making sure the vendor data behind those forms is complete, correct, and ready before the deadline week starts. Forms 1099 can be filed on paper by March 2, 2026, or electronically by March 31, 2026, while Form 1099-NEC had an earlier due date of February 2, 2026.

That distinction matters because teams often lump every 1099 into one deadline conversation. That is how they end up using the wrong due date, rushing corrections, or realizing too late that a contractor record is missing a taxpayer identification number. If you are publishing this during the week of March 9, the countdown is real. But the smart move is not panic. It is triage. Week 22 getw9 – March 9th

The IRS general instructions say that, except for listed exceptions, Forms 1097, 1098, 1099, 3921, 3922, and W-2G are due by March 31, 2026 if filed electronically. The same instructions say those returns were due by March 2, 2026 if filed on paper, and that Form 1096 must accompany paper submissions.

So if your business is filing most standard 1099 forms electronically, March 31 is the date you care about. But “most” does not mean “all.” That is where people get sloppy. Sloppy is expensive in tax compliance.

Form 1099-NEC is the main exception that trips people up. The IRS instructions say Form 1099-NEC was due by February 2, 2026, whether filed on paper or electronically. It does not wait for March 31.

That means a business paying contractors for nonemployee compensation cannot treat March 31 as a universal 1099 deadline. If you paid independent contractors and that income belongs on 1099-NEC, the filing date was earlier. A late-March scramble will not fix a missed early-February obligation. What late March can still affect is your filing quality, corrections, and any other eligible information returns still moving through your process.

The deadline itself is not the real problem. The real problem is weak vendor records.

A filing team can know the date perfectly and still fail because the legal name does not match the TIN, the wrong form was collected, the vendor record is incomplete, or someone assumed a PDF in an email thread counted as a usable process. The IRS makes clear that incorrect or missing TINs can create penalties and backup withholding issues.

In other words, late-March pain usually starts months earlier.

A lot of small businesses still think electronic filing is only required at a high volume. That is outdated thinking. The IRS reduced the threshold, and businesses filing 10 or more information returns in the aggregate generally must file electronically. The current rule is not 250 returns by form type anymore. It is 10 in aggregate.

That matters because some teams still build a paper-first process and only realize too late that they should have been planning for e-file. If you are near or above that threshold, waiting until the last two weeks of March to sort this out is bad planning, not bad luck.

Form W-9 is how a payee gives the requester the correct TIN for information reporting. The IRS says Form W-9 is used to provide the correct taxpayer identification number to the person who must file an information return.

Before you chase vendors, make sure your team knows what a completed W-9 should include

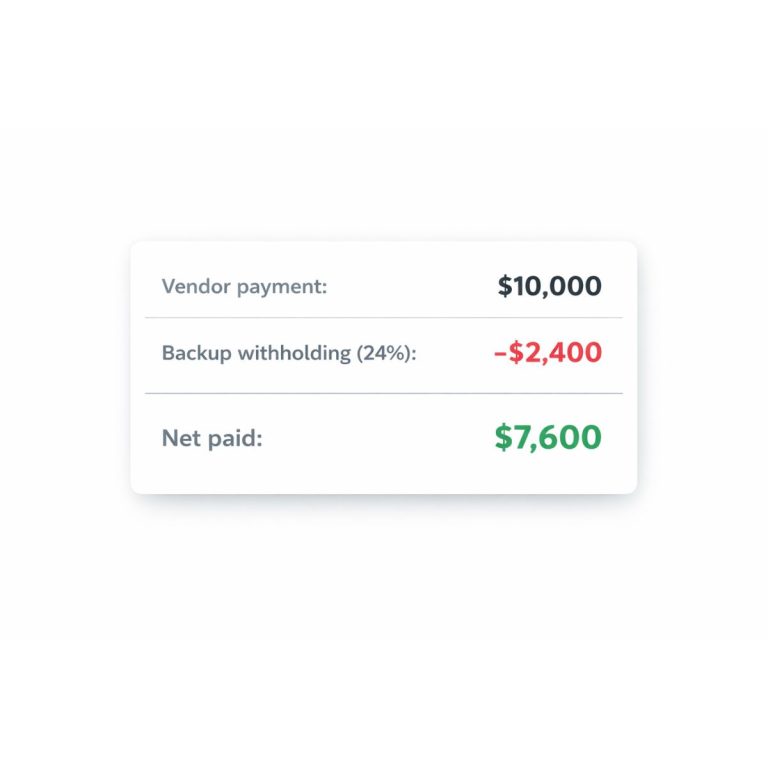

If a payee does not provide a TIN, the IRS says the TIN box on the information return may be left blank, but backup withholding may apply. The instructions also say that if a TIN is not furnished in the required manner, withholding may apply until the TIN is provided.

This is where a lot of businesses fool themselves. They think, “We can file now and clean it up later.” Maybe. But corrections cost time, and if the record was weak to begin with, the correction process is rarely quick.

Having a W-9 on file is not the same as having a correct record. The IRS says an incorrect or missing TIN can lead to penalties, and if the IRS notifies you that the payee’s TIN is incorrect, you may need to furnish a B notice and withhold on reportable payments after the required window.

That means your real question is not “Do we have a form?” It is “Does the name, entity type, and TIN on the record support filing?” Those are not the same thing.

This is exactly why vendor records should be checked before filing season turns into cleanup season.

Your social file includes a W-9 versus W-8 theme, and it is a useful reminder even though it should not be the primary keyword target for this post. The IRS says a U.S. person generally uses Form W-9, while a foreign individual generally gives Form W-8BEN to establish foreign status and, if applicable, claim treaty benefits or a reduced rate of withholding. The W-8BEN instructions also say failure to provide it when requested may lead to withholding at 30% or the backup withholding rate in some cases. Week 22 getw9 – March 9th

This matters because businesses often discover the wrong form problem during onboarding, but they feel the pain during filing. By then, the record is already in your system, the vendor may already have been paid, and your team is now untangling what should have been handled upfront.

If your team is in the week-of-March-9 window, do this in order.

First, pull the full list of vendors or payees tied to reportable payments. Do not work from scattered inboxes or individual team members’ folders.

Second, split the list into three buckets:

Third, review questionable records for legal name, tax classification, and TIN format. If the record looks incomplete, treat it as incomplete. Optimism is not a control.

Fourth, confirm whether your volume means you must e-file. For many businesses, the answer is yes, and pretending otherwise this late in the cycle wastes time. The IRS says 10 or more information returns in aggregate generally triggers mandatory e-filing.

Fifth, separate 1099-NEC thinking from March 31 thinking. That deadline was February 2, 2026. Do not mix the timelines.

Sixth, fix vendor data now instead of assuming correction files will save you later. They can help, but correction work is still work.

Most compliance problems do not come from one dramatic error. They come from a chain of ordinary neglect.

Someone onboarded a vendor without the right form.

Someone accepted a name that did not match the tax record.

Someone assumed a paper process would be “good enough.”

Someone waited until the deadline month to ask whether the data was usable.

That is not an IRS problem. That is a workflow problem.

And workflow problems are exactly what AP teams keep repeating because nobody wants to stop and fix the intake process when there is immediate work to do. That is the trap.

A better process starts before filing season.

You request the tax form at onboarding, not after payment. You store the completed record in one place, not across email chains. You track what has been received and what is still missing. You review records for completeness before reporting season compresses the timeline. And you keep a clean trail of who submitted what and when.

That is not flashy. It is just competent.

The social asset in your weekly file that says “send a link and track what’s received” is not enough to carry a whole article on its own, but the operational idea behind it is sound: collection has to be structured, visible, and repeatable if you want cleaner filing outcomes. Week 22 getw9 – March 9th

GetW9 should be positioned here as the tool that helps businesses collect vendor tax information earlier and keep it organized before the deadline crunch.

Not as magic. Not as “stress-free compliance” fluff. Just as a practical system for requesting W-9s, tracking status, and reducing the usual mess created by inbox-based collection. That is a stronger claim because it is believable.

If your team is staring at March 31, the real win is not merely submitting on time. The real win is avoiding the bad record that forces corrections, notices, and extra work later.

The March 31 1099 e-file deadline matters, but the date itself is only half the story. The other half is whether your vendor records are ready.

For 2026, the IRS says most eligible 1099s were due by March 31 if e-filed, most paper filings were due March 2, and 1099-NEC was due February 2. The IRS also requires electronic filing for many businesses once they hit 10 information returns in aggregate.

So the question for AP teams is simple: are you using the rest of March to file, or are you using it to clean up problems that should have been fixed before March even started?

That answer tells you more about your compliance process than the deadline ever will.