Physical Address

5206 Hwy 5 N Suite 100, Bryant, AR, United States, Arkansas

Physical Address

5206 Hwy 5 N Suite 100, Bryant, AR, United States, Arkansas

A lot of businesses ask the wrong question.

They ask, “Do we need to collect a new W-9 every year?”

That is not the real issue.

The real issue is whether the W-9 you already have is still accurate enough to rely on for reporting, vendor records, and backup withholding decisions. The IRS currently lists Form W-9 with a January 2026 revision, and the requester instructions make clear that name/TIN mismatches, address updates, and backup withholding notices all matter operationally.

A W-9 does not become “bad” because January arrived. It becomes bad when the facts behind it changed.

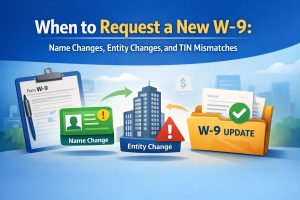

Request a new W-9 when the vendor’s tax identity, reporting details, or withholding status may no longer match what you have on file.

That includes obvious cases like a legal name change. It also includes less obvious cases, like a TIN mismatch notice, a tax classification change, or a vendor who quietly changed how they operate. Competitor content from Tax1099, Tipalti, and AP Now all point to the same operational truth: the trigger is not the calendar, it is the change in circumstance.

If the vendor’s legal name changed, your old W-9 is now risky.

That matters because the IRS compares the name/TIN combination on the information return to its records. The requester instructions also say that if the payee marks the address as “NEW,” you should update your records. In practice, if the vendor gives you a new legal name, new DBA situation, or new mailing identity, you should not keep trusting the old form.

Examples:

This is where teams get sloppy.

A vendor may still look like “the same vendor” in your system, but their tax classification may have changed underneath. A sole proprietor may form an LLC. A single-member LLC may elect a different tax treatment. A business may move from disregarded-entity treatment to corporation treatment.

That is not cosmetic. That changes what should appear on the W-9 and can affect reporting treatment. Tax1099 and Tipalti both flag entity and legal-form changes as reasons to refresh the form, and that lines up with common AP best practice.

If the taxpayer identification number changed, stop pretending the old W-9 is still usable.

IRS general instructions state that for information returns, sole proprietors who are not otherwise required to have EINs should use their SSNs. That means TIN handling for sole proprietors can get messy when a vendor starts using a different identifier, forms a new entity, or gives inconsistent tax information across systems.

This is the exact kind of issue that creates downstream filing errors, confusion, and backup withholding headaches. Running TIN Matching before filing helps catch bad name/TIN combinations before they turn into notices.

This is not optional workflow cleanup. This is where people get burned.

The IRS says that when a payee appears on a CP2100 or CP2100A notice for the first time, the payer must send the First B Notice and a Form W-9. The IRS also says a name/TIN mismatch notice means the information return filed does not match IRS records.

So if you receive:

you should treat the old W-9 as suspect and re-solicit promptly.

A lot of teams underestimate this one because an address feels “administrative.”

It is not. The IRS requester instructions explicitly tell you to update your records if the payee marks their address as “NEW.” And from an operations standpoint, a changed address is often a warning sign that other details may have changed too. AP Now goes even further: if the vendor notifies you of changes like address or banking details, that is a smart time to request a fresh W-9 because those updates often come alongside a broader change in circumstance.

This is not an IRS line-item rule. This is disciplined operations.

If a vendor has been inactive for a long time, then reappears with a new invoice, new remittance details, or new contact info, do not blindly rely on the form you collected years ago. That is how stale vendor masters survive until filing season exposes them.

This is where good teams separate themselves from chaotic teams:

Not automatically.

The IRS instructions focus on having correct, current payee information and on re-soliciting after mismatch problems. They do not describe a mandatory annual refresh cycle. The smarter rule is: refresh when the facts changed, when a mismatch notice appears, or when the record is old enough that relying on it is just wishful thinking. That is consistent with how Tax1099 and AP-focused guidance frame the issue.

Before the next vendor payment run, review vendors for these triggers:

If any one of those is true, request a fresh W-9.

Knowing the triggers is easy. Catching them consistently is the hard part.

GetW9 is useful because it turns W-9 collection into a repeatable workflow: send a secure request, track status, follow up automatically, and save completed W-9 PDFs with submission history. That is much better than depending on inbox archaeology and memory.

The wrong habit is asking for a new W-9 every January with no thought behind it.

The better habit is knowing exactly when the old W-9 stopped being reliable.

That is the real job: not collecting forms for the sake of forms, but keeping vendor data accurate enough that January does not turn into repair work.

If your team cannot quickly tell which vendors need a refreshed W-9, your process is weaker than you think.