Physical Address

5206 Hwy 5 N Suite 100, Bryant, AR, United States, Arkansas

Physical Address

5206 Hwy 5 N Suite 100, Bryant, AR, United States, Arkansas

Last updated: April 19, 2026 revised for OBBBA $2,000 1099-NEC threshold, January 2026 draft W-9 changes, and current IRS penalty tiers.

The W-9 and 1099 playbook usually starts the same way: it’s late January, your team is tired, and someone asks a simple question “Do we have W-9s for everyone who needs a 1099?” That’s when the calm disappears. You open the vendor list and see missing forms, duplicate vendors, and names that don’t match what’s on file. Suddenly, you’re not doing accounting work anymore. You’re doing detective work.

And here’s the annoying part: the stress isn’t caused by tax season. Tax season just exposes the gaps you already had.

This post is a clean W-9 and 1099 playbook you can use right after the deadline rush so you don’t repeat the same pain next year.

📌 2026 Updates to This Playbook

Three things changed in 2026 that directly affect how AP teams should run the W-9 and 1099 process:

Before getting into the playbook rules, two regulatory changes are worth understanding clearly. They don’t change what you do — they change the math on why it matters.

OBBBA raised the 1099-NEC reporting threshold from $600 to $2,000 for payments made in 2026. Some AP teams read that and relax. That’s a mistake for two reasons.

First, you can’t always tell at onboarding which vendors will cross $2,000 this year and which won’t. A contractor you use for a single $800 project in Q1 becomes a $4,500 vendor by Q3. If you only collected a W-9 from “the ones who’d hit the threshold,” you’re now chasing in December.

Second, backup withholding still applies to payments where the payee hasn’t provided a valid TIN — regardless of whether you end up issuing a 1099. A missing or wrong TIN still triggers 24% withholding on the payment, and that obligation exists independent of the $2,000 line.

Translation: keep collecting W-9s at onboarding for every new vendor. The threshold change cleaned up the filing side, not the collection side. (Full analysis of the OBBBA change →)

The IRS released a draft Form W-9 in January 2026 with two substantive changes:

If you have older W-9s on file from sole proprietor vendors listing an EIN, those records are not automatically invalid — but new collections and re-collections should follow the draft form’s rules. Any vendor record you touch during cleanup this year should be refreshed if it was filled out under the old sole-prop convention. (Full walkthrough of the 2026 draft W-9 →)

The current IRS information return penalty structure for 2026 filings:

| When you correct it | Penalty per form (2026) |

|---|---|

| Up to 30 days late | $60 |

| 31 days late through August 1 | $130 |

| After August 1 or not filed | $340 |

| Intentional disregard | $680 (no maximum) |

These apply per form and are cumulative. An AP team with 120 contractors and sloppy records can reach five figures of exposure without trying. That’s the real cost the playbook below is designed to prevent. (IRS penalty reference, last reviewed Feb 2026)

Let’s talk about “Nina.”

Nina runs AP. She’s sharp. She cares. She follows up.

Still, January turns into a mess.

Here’s what happened:

Nina didn’t fail. The system failed Nina.

This is the core issue: you don’t have one trusted source of vendor truth.

Instead, you have a vendor record, a spreadsheet, an email thread, and a folder called “W9s (new new).”

That’s why this W-9 and 1099 playbook matters.

If you’re still chasing forms right now, read: “Missing W-9s in January? The Late-Filer Survival Guide (With Copy-Paste Email Templates)”

If collecting a W-9 is optional, vendors treat it like optional homework.

Duplicates create confusion, wrong totals, and name/TIN mismatches.

Invoices often show a DBA. The IRS wants the legal name tied to the TIN.

Email is not a filing cabinet. It’s a maze.

When “everyone” owns W-9 collection, nobody drives it to completion.

This is the easiest win. You don’t even need to start with “no W-9, no pay.” Start with: we don’t activate a vendor until the W-9 is received (or the correct form if they aren’t a U.S. vendor). This one rule removes 70% of the January scramble — and it’s the cheapest insurance against the IRS penalty ladder for missing or incorrect information returns: $60 per form if filed up to 30 days late, $130 if filed 31 days late through August 1, $340 if filed after August 1 or not filed at all, and $680 per form for intentional disregard (2026 figures, with no maximum on intentional disregard). On a vendor list of 80 contractors, one missed W-9 cascade is a five-figure hit. (IRS information return penalties)

Email creates:

Most teams clean vendor data when panic is already high.

Flip it. Do a cleanup when you’re calm, not when you’re rushed:

Vendors respond when your process is clear.

A simple ladder works:

Keep it polite, but make it real.

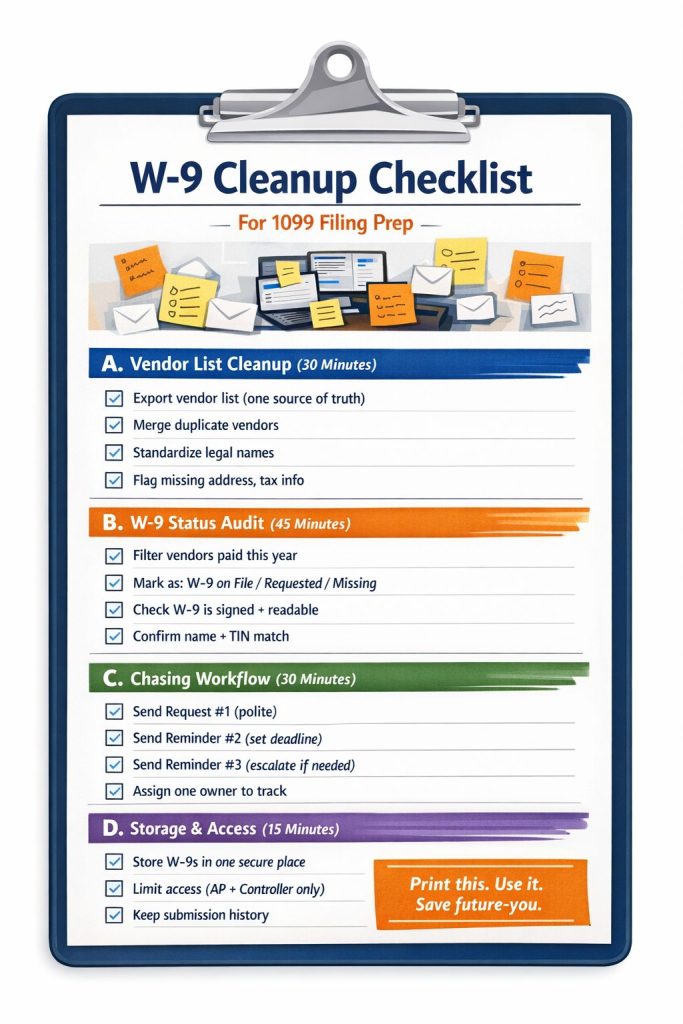

Use this checklist as your “post-season reset.” It’s short on purpose.

This checklist is a core part of the W-9 and 1099 playbook because it turns chaos into steps.

Run this meeting right after the busy week, while the pain is fresh:

Write the answers down. Otherwise, you’ll repeat the same season.

It applies to payments made in 2026 and later. Your January 2026 filing (reporting 2025 payments) still uses the $600 threshold. Starting with 2026 payments, the $2,000 threshold takes effect for 1099-NEC reporting.

Not automatically. Existing W-9s aren’t retroactively invalid. But any vendor record you update, verify, or refresh during 2026 cleanup should follow the new draft form’s rules, sole proprietors use SSN, not EIN. It’s a good idea to build re-collection into your standard annual refresh rather than triggering a mass re-request.

No. Backup withholding obligations, vendor record accuracy, and audit readiness all depend on having a valid W-9 on file regardless of whether a 1099 ends up being issued. Skipping the W-9 is a false economy.

The IRS issues a CP2100 or CP2100A notice, which starts the B-Notice clock. You have specific response timelines — typically 15 business days — and failure to follow through triggers backup withholding on future payments. Full walkthrough of the response process.

At onboarding for every new vendor, and again in a batch run each October before Q4 closes. October is late enough to catch most of the year’s changes but early enough to fix issues before January. How TIN matching works.

If your W-9 process is spreadsheet + email chasing, you’re choosing stress on purpose.

GetW9 makes the W-9 and 1099 playbook easier to run because it gives you:

The goal isn’t “more software.”

The goal is a process that doesn’t collapse in January.

The teams who stay calm in tax season aren’t “more disciplined.” They’re more prepared. 2026 made that gap bigger, not smaller. A higher threshold doesn’t mean less documentation, it means the same W-9 work with fewer 1099s at the end, and the same penalty exposure when a record is wrong. Use this W-9 and 1099 playbook now, right after the rush, so next year you can answer that scary January question without hesitation: “Yes. We’re good. It’s already handled.”